7 Accounting Mistakes That Quietly Cost Growing Businesses in India (And How to Fix Them)

- Admin

Jun 16, 2026

Jun 16, 2026- Accounting

Most businesses don't fail because of one big financial disaster. They bleed slowly — through missed input tax credits, late filing penalties, unreconciled books, and decisions made on outdated numbers.

At Ledger Lions, we've spent over 15 years working with startups, family-owned businesses, and enterprises across industries. And whether it's a film production house managing multi-currency payments or a family business that's grown faster than its systems, we keep seeing the same avoidable mistakes.

Here are the seven most common ones — and what to do about them.

1. Mixing personal and business finances

This is the classic trap for founders and family businesses. The owner pays a vendor from a personal account, withdraws cash for household expenses from the business, and figures, "We'll sort it out later."

Later never comes. At year-end, your accountant spends days untangling transactions, your books don't reflect the true health of the business, and you may end up with avoidable tax complications around director loans and drawings.

The fix: Separate bank accounts and cards from day one. Every rupee that moves between you and the business should be documented — as salary, drawings, or a loan.

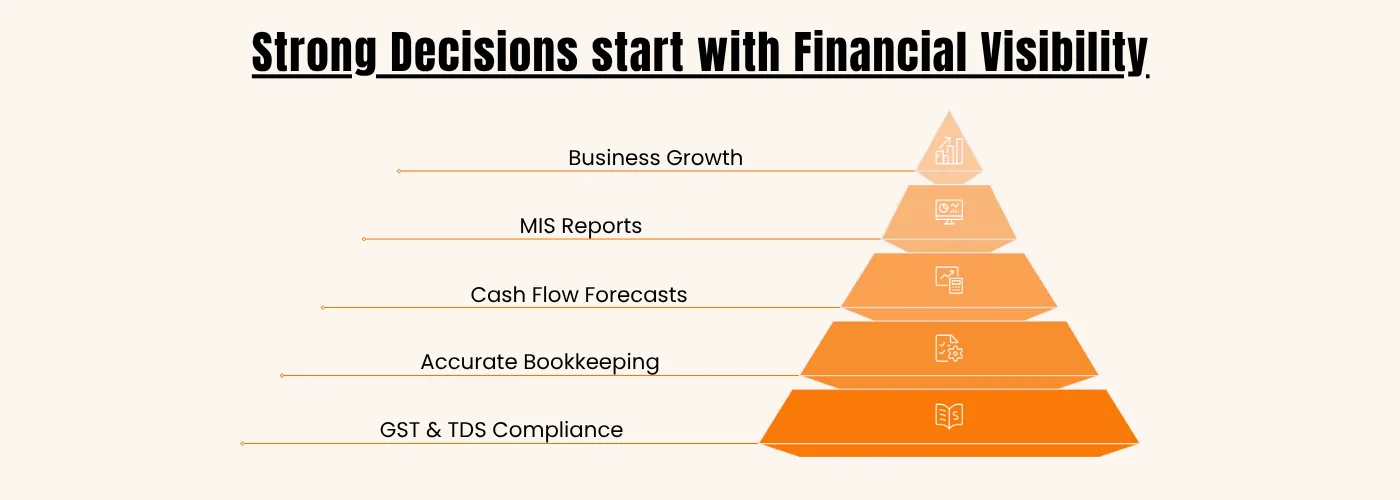

2. Treating GST compliance as a month-end scramble

Many businesses file GSTR-1 and GSTR-3B on time but never reconcile their purchase records with GSTR-2B. The result? Missed input tax credits that are pure money left on the table — or worse, claimed credits that don't match your suppliers' filings, inviting notices from the department.

The fix: Monthly reconciliation between your books, GSTR-2B, and vendor invoices. If a supplier hasn't uploaded an invoice, follow up before the credit lapses, not after.

3. Ignoring TDS until the notice arrives

TDS is one of the most common areas where growing businesses slip. Payments to contractors, professionals, rent, and even certain purchases attract TDS — and the rules change often enough that what was correct last year may not be this year. Interest, late fees, and disallowance of expenses under Section 40(a)(ia) add up quickly.

The fix: Build TDS checks into your payment process itself, not your quarterly filing process. Every vendor payment should pass through a simple question: does this attract TDS, at what rate, and is the PAN on file?

4. Running the business on bank balance instead of cash flow

"There's money in the account, so we're fine" is how profitable businesses run into cash crunches. Your bank balance doesn't show the GST payment due next week, the salaries due at month-end, or the customer payment that's already 60 days overdue.

The fix: A simple rolling cash flow projection — even 8 to 12 weeks ahead — changes how you make decisions. You'll know in advance when to chase receivables harder, delay a discretionary purchase, or arrange working capital.

5. Getting MIS reports that arrive too late to matter

Many business owners receive their profit and loss statement three months after the quarter ends — at which point it's history, not information. You can't course-correct on numbers you see too late.

The fix: Monthly MIS reporting with a fixed deadline — ideally within 10 to 15 days of month-end. It doesn't need to be elaborate. Revenue, gross margin, expenses against budget, receivables aging, and cash position cover most of what an owner needs to act on.

6. Forgetting ROC and Companies Act compliance

For private limited companies, compliance doesn't end with tax. Annual filings like AOC-4 and MGT-7, board meeting requirements, DIN KYC, and event-based filings (changes in directors, share capital, registered office) all carry penalties — and unlike many tax penalties, ROC late fees accumulate per day with no upper cap on some forms.

The fix: Maintain a compliance calendar that covers MCA deadlines alongside GST and income tax. Better still, have one team accountable for the full picture so nothing falls between two stools.

7. Outgrowing your accounting setup without noticing

The Tally file and part-time accountant that worked at ₹50 lakh turnover starts breaking at ₹5 crore. Invoicing gets delayed, approvals happen on WhatsApp, and nobody is quite sure which version of the books is current. The cost isn't just inefficiency — it's the strategic decisions you're making without reliable numbers.

The fix: Periodically ask whether your accounting systems match your scale. Sometimes the answer is better software and automation. Sometimes it's a structured outsourced accounting team. And when you need financial strategy — pricing, expansion, funding readiness — but can't justify a full-time CFO's salary, a Virtual CFO gives you that expertise on demand.

The common thread

None of these mistakes happen because business owners are careless. They happen because owners are busy building the business — and accounting quietly slips from "managed" to "managed somehow."

The businesses that grow smoothly are the ones that treat accurate books and proactive compliance not as a year-end formality, but as the foundation for every decision they make.

If any of these seven points hit close to home, it might be time for a conversation. At Ledger Lions, we help businesses move from firefighting to clarity — with accurate accounting, dependable compliance, and Virtual CFO support that scales with you.